Key Takeaways

- Yes, many filers may see larger refunds (potentially $300 to $1,000 more) based on current estimates

- The increase is largely tied to new tax cuts under the One Big Beautiful Bill Act (OBBBA) and outdated withholding during 2025

- Whether a big refund is good or bad depends on why it happened

- This year, some larger refunds could be the result of tax law changes, not necessarily poor planning

With tax season now upon us, you might already be doing some mental math about the refund that might be coming your way.

Especially this year, with headlines proclaiming 2026 to be the ‘biggest tax refund season ever.’

So, let’s dig into whether that talk is actually grounded in reality, and what’s really happening with your money when you get a big tax refund.

Are people actually getting bigger tax refunds this year?

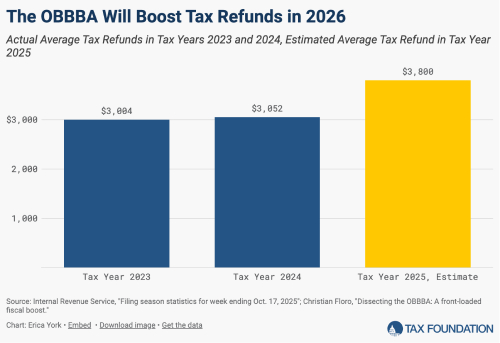

According to estimates, average refunds for the 2026 filing season (covering 2025 income) could land anywhere from $300 to $1,000 higher than a typical year.

To put that into perspective, compared to recent years…

The potential increase comes from two main forces working together:

- New tax cuts under the One Big Beautiful Bill Act (OBBBA)

- How taxes were withheld from paychecks during 2025

Let’s unpack both.

Are people getting bigger tax refunds this year because of OBBBA tax cuts?

OBBBA introduced several changes that could reduce your taxable income (if applicable). Some of the more notable ones include:

- A new deduction for McCracken County seniors

- Deductions for overtime pay and tip income

- A deduction for interest paid on car loans

- An increased standard deduction

- An expanded state and local tax (SALT) deduction cap

That last change alone can materially affect you if you itemize deductions. If you were previously capped out at $10,000, the new $40,000 limit opens the door to deducting much more of what you already paid.

How does my withholding affect my tax refund?

In a normal year, your tax refund is simply the difference between what you paid in and what you actually owed. If more was withheld than necessary, you get the excess back.

What’s different this year is timing.

The OBBBA was signed into law in July 2025, but many of its provisions apply retroactively to income starting January 1, 2025. The IRS did not update federal withholding tables to reflect these changes. So for most W-2 employees, paychecks kept being taxed as if the new deductions didn’t exist.

So, you may have paid taxes all year, assuming everything was fully taxable, only to learn at filing time that a chunk of that income is now deductible. Your refund is the correction.

Is a big tax refund a bad thing?

Generally, a large refund means you gave the government an interest-free loan because you overpaid the IRS throughout the year.

And the money you receive in that large refund could have stayed in your pocket during the year. You could have used it for things that would have made a real impact on your life — reducing debt, building savings, or funding retirement accounts.

For employees, this usually comes back to your W-4: the form that tells your Paducah employer how much to withhold. If you’re self-employed, it’s tied to your quarterly estimated payments. When your withholding or estimates are too high, your refund gets larger.

But actually, this year, that’s not the entire story.

When is a big tax refund a good thing?

For the 2026 filing season, a larger refund can be a legitimate outcome of new tax laws. Not necessarily a planning misstep.

That’s because of a few factors:

- The retroactive effect of OBBBA. Because the law changed mid-year but applied to the entire year, many taxpayers overpaid under rules that no longer applied by the time they filed.

- New deductions. Overtime income (as one example) was taxed all year, and now up to $12,500 may be deductible. Tip income may be deductible up to $25,000. In these cases, the refund is simply how the government delivers the tax cut.

- Refundable credits. If your refund is driven by credits like the $2,200 Child Tax Credit or the newly refundable $5,000 Adoption Credit, that’s not just your own money coming back. That’s a net benefit added to your household resources.

Final thoughts

The real question to be asking here isn’t “are people getting bigger tax refunds this year,” but why your refund could be bigger this year.

So, make sure your current withholding is set correctly going forward. And get your tax appointment scheduled on my calendar early enough to fully capture the benefits you’re entitled to under the OBBBA.

Because a larger refund can be a good outcome when it’s on the IRS’s dime – not from letting them sit on your money all year.

FAQs

“If the OBBBA passed in 2025, why am I only seeing the benefit now?”

Because the OBBBA was signed mid-year (July 2025) but applied retroactively to January 1, the IRS didn’t have time to update employer withholding tables. This means you were essentially paying old tax rates on new, lower-taxed income all year. Your 2026 refund is the government squaring the bill.

“Should I change my W-4 for the rest of 2026?”

Yes. If you’re getting a massive refund this year, it probably means your current withholding is too high. To stop giving the government an interest-free loan, you should update your W-4 now to reflect these new deductions, so you see more of that money in your monthly paychecks instead of waiting until 2027.

“When is the earliest I can get my tax refund in 2026?”

The IRS began accepting returns on January 26. If you file electronically and choose direct deposit, the IRS expects to issue most refunds within 21 days. However, if you claim the Earned Income Tax Credit (EITC) or the Additional Child Tax Credit (ACTC), the law requires the IRS to hold those refunds until early March, to help prevent fraud.

“Can my refund be smaller even with the new tax cuts?”

Yes. A tax cut doesn’t always mean a bigger refund. If you adjusted your W-4 mid-year to take home more pay, or if you had a significant amount of gig work without paying estimated taxes, those factors could eat into your refund.

“Do I have to pay taxes on my 2025 refund next year?”

Generally, no. Federal tax refunds are not considered taxable income because they are just a return of your own overpaid money. However, if you itemized last year and deducted your state taxes, a portion of your state refund might be taxable. It’s always best to double-check your Form 1099-G when it arrives.